Tax reform has certainly shaped up to be a massive change in our tax code that will keep all of us quite busy for years to come. This means new opportunities and loopholes for your CPAs to start thinking about for you. Although the following analysis may seem lengthy, this is hundreds of pages shorter than the actual new tax code. Before we get into the nuts and bolts of the law, there are a few things you can do before December 31, 2017 and in early 2018 to take advantage of the upcoming rule changes.

Things To Do by December 31, 2017

- Pay Property Taxes and State and Local Taxes – This is an area where there is dramatic change coming in 2018. Starting next year, you can only deduct a combined total of $10,000 for your state income tax and property tax. For most of our clients, this will result in a reduction of what can be deducted as part of the itemized deductions.

- If your home property taxes have not been paid, we strongly suggest you go ahead and pay these taxes before December 31, 2017. If you have escrow, call your mortgage company to make sure it is paid this year. Otherwise, you can complete the payment online or write a check.

- Even though the 4th quarter estimated state tax payments are not due until January 15, 2017, you should make sure to pay them before December 31, 2017. Whether it is beneficial or not depends on your AMT tax status, so please feel free to contact us. You are specifically not allowed to prepay your 2018 taxes to get a deduction in 2017.

- Business Owners: Accelerate Payments/Delay Revenue Collection – Depending on your income, accelerating payments to vendors or delaying revenue collection could be a good strategy to reduce your taxes over multiple years. The tax brackets are lower starting next year, so a deduction this year is possibly more valuable, and revenue taxed next year would cost less in tax liability. This is a very complex area with other considerations, such as pass-through deductions beginning 2018, so you should discuss this with us.

- Complete Charitable Donations – Although the tax break for charitable contributions is one of the few itemized deductions retained, other changes will reduce its usefulness for some. The only way to take advantage of the charitable deduction is to itemize your deductions. With the increased standard deduction and many of the other itemized deductions disappearing next year, itemizing deductions will not make sense for many people who have done so in the past. That said, there are ways that you can continue to contribute to the charities that you love while still retaining some of the tax benefit. One is to complete your charitable deductions this year, or possibly consider using a donor advised fund (DAF). In a nutshell, a DAF allows you to take a charitable deduction in the year that you make the contribution to the DAF. Once the DAF is funded, you can request that the money in the fund be granted to charities now or in the future, using whatever time period for the distribution of the funds to charities that you wish. You can even use appreciated stock to contribute. For example, let’s say you have an investment you have owned for a long time that you bought for $1,000 and is now worth $2,000. You can open a DAF, contribute the investment without selling it (thus, avoiding capital gains taxes) and take a $2,000 deduction this year.

- Pay Miscellaneous Deductions – Starting next year, no miscellaneous deductions, such as unreimbursed job expenses, home office deductions, accountant fees will be deductible. If you have any outstanding bills here, we would suggest you pay them by year end.

Things To Do in Early 2018

- Review Retirement Plan Contributions – Due to the possibility of a lower tax bracket, it may make sense for you to change your retirement plan contributions to after-tax Roth ones versus pre-tax contributions. This requires detailed analysis of your tax situation, so please contact us.

- Review Home Equity Line of Credit – Going forward, interest on these loans will no longer be deductible for non-acquisition, non-home improvement uses. We would recommend you pay these down, combine them into a primary loan by refinancing, or use a margin loan on your investments to continue the deduction.

Overview of Tax Reform

Our opinion of the overall tax reform is that it primarily benefits large corporations by allowing them to receive a 40% tax bracket reduction (from 35% to 21%), which makes them more globally competitive. The idea is for corporations to have an incentive to do business in the U.S., which results in domestic job and wage growth. However, to pay for these tax cuts, some corporate loopholes have been closed, and numerous individual deductions and credits have been curtailed. Of course, some of the tax cuts may end up being financed by additional national debt. On the corporate side, deductibility of debt has been reduced (except for commercial real estate investors and developers), which will raise tax revenue for the government. On the individual side, mortgage debt interest deductibility has also been reduced. Previously, interest on a mortgage up to $1 million was deductible. Homeowners may only deduct interest on the first $750,000 of their mortgages starting in 2018.

The law clearly has both winners and losers. Taxpayers with similar incomes who live in different parts of the country will have different tax outcomes. People in states with higher income taxes, such as NY, CA, NJ, IL, CT, may see a federal tax increase due to the reduction in the deductibility of these state taxes, and a taxpayer with the same income in other states may see a federal tax decrease. Also, certain industries have been favored over others with tax cuts. High capital-intensive businesses, like manufacturing, will get a large tax reduction, but service businesses, such as law, medicine, finance/accounting, consulting, will not get a tax reduction. It is this sort of uneven picking of winners and losers that will create more loopholes and opportunities for taxpayers. To add to the complexity, the majority of the tax reductions and changes for individuals disappear in 2025, but the corporate tax cuts will be permanent.

Individual Tax Reform Highlights and Changes

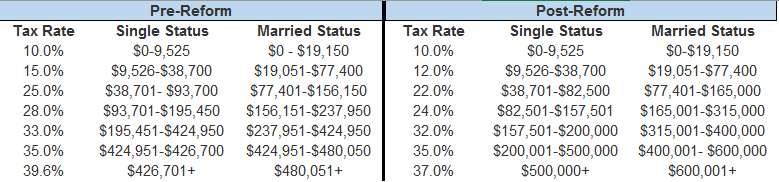

- Almost all tax brackets will decrease in 2018. For example, the current 2017 law has a maximum tax bracket of 39.6%; the new tax law will reduce this bracket down to 37%. Here is a comparison of the brackets from 2017 to 2018:

- Standard Deduction – As a taxpayer you can currently deduct the higher of your actual deductions (itemized deductions) or the standard deduction. Currently, the standard deduction is $13,000 (married) and $6,500 (single) and under the new law the deduction is $24,000 and $12,000, respectively. The result of reduced itemized deductions and the increased standard deduction is a simplified tax filing for millions of taxpayers.

- Personal Exemptions – The current law allows a personal exemption of $4,150 per person in the household. This is repealed going forward. A new expanded child credit with larger income thresholds and different age requirements will take its place. The child credit will not apply for dependents over 17, but the personal exemption did. So, taxpayers with larger families and/or older children will see less tax relief under this change.

- Child Tax Credit – Currently there is a $1,000 child credit with income phaseouts at $75,000 and $200,000 for married/single filers. This changes to $2,000 with income phaseouts at $110,000 and $400,000 for married/single filers. This is certainly an increase and more people will be eligible due to the higher income phaseouts.

- Alternative Minimum Tax (AMT) – This has been changed so that it only affects people with income over $1,000,000 (for married couples) and $500,000 (for single filers). AMT was typically triggered by state and local tax deductions, but with these deductions reduced along with the higher threshold, very few people will be subject to this tax.

- Alimony – Currently, alimony payments are an above-the-line deduction for the person making the alimony payment, which means they are tax free to the payer. This alimony deduction is repealed for divorces carried out after December 31, 2018. The new rule does not affect anyone already paying alimony.

- 529 Plans – Starting in 2018, 529 plans will be expanded to allow for tuition payments to private schools, religious schools, etc. From a planning standpoint, parents with young children can plan to contribute to these for pre- and post-secondary education from an early age (but not for home schooling). For parents with older kids, the tax-free status of the 529 may not be a significant advantage for children in pre-secondary education.

- Estate Taxes – The estate tax exemption is doubled to $11.2 million (inflation-adjusted) per taxpayer from the current law of $5.1 million (inflation-adjusted). However, like most of the individual tax changes, this provision is only valid until 2025 when it reverts back to current law. We saw this in previous administrations, and the increase is a welcome change for many, but planning is more complex than ever due to the sunset provisions in 2025.

Business Tax Reform Changes and Highlights:

- Pass-Through Entities – One of the largest changes in the tax code deals with entities or sole proprietorships that pass through income to their individual owners. This includes entity types, such as LLCs, S-Corps, LLPs. This is a very complex change, which will require detailed planning and understanding. Overall, businesses will be allowed a 20% deduction of income which is applied to the owner/shareholder. This is based on the capital employed in the business, the shareholder’s wages and other wages paid, the amount of taxable income, and the industry. Some service businesses are exempt from this, but there was a last-minute change to allow architects and engineers to have preferential treatment.

- Meals and Entertainment – Meals will generally continue to be deductible at 50%, but entertainment such as clubs for social purposes, sporting event tickets will no longer be deductible.

- Business Use Vehicles – Currently, luxury vehicles have their deduction capped by low amounts of annual depreciation. A $50,000 car may take 10 years to deduct, under current law. However, going forward, these limits have been dramatically increased (almost tripled).

- Section 179 – This deduction has been raised from $500,000 to $1,000,000, and some real property may now qualify for this deduction. This could help businesses offset the cash outflow of large purchases with an immediate deduction.

- C-Corp – Non-pass through corporations will see a dramatic tax rate reduction from 35% down to 21%.

What Didn’t Change:

- Capital Gains Tax Rates – They stay the same at 15%/20% depending on your income. Obamacare taxes of 3.8% continue to apply as the net investment tax.

- Teachers Expenses – The Senate bill had eliminated these, but no changes were made in the final bill.

- Specific Lot Identification– The Senate bill would have forced investors to sell investments with the worst tax outcome (called FIFO lot identification). This never made it into the final tax bill.

- Capital Gain Exclusion for Primary Residence – You are still allowed to exclude up to $500,000 from the gain on the sale of a primary home. Taxpayers must own and use the house for the last two out of five years.

We would anticipate more guidance will come from the IRS on the ambiguous areas over the years, but meanwhile CPAs will have a lot of opportunities to help their clients. This was one of the largest tax law changes since the Reagan era and will impact all individual and corporate taxpayers. We suggest you talk to us for help navigating the complex changes and to take advantage of any opportunities these changes will create.

If you would like to discuss wealth planning strategies in order to maximize your tax benefits, we suggest you contact Redwood Wealth Management. They are a fee-only independent advisory firm. Their website is www.redwoodwm.com where you may find their contact information.

We wish you a prosperous and healthy new year!

Segars & Vora, CPA's